Insights

Achievement-based prompts significantly increased engagement:

12% clickthrough vs. 6.5% baseline.

Higher re-deposit rate (42.18%) and faster follow-up actions.

Small nudges like framing success or offering planning tools helped overcome inertia.

Results demonstrated that behavioral science can help improve digital financial behaviors at scale.

Methods + Approach

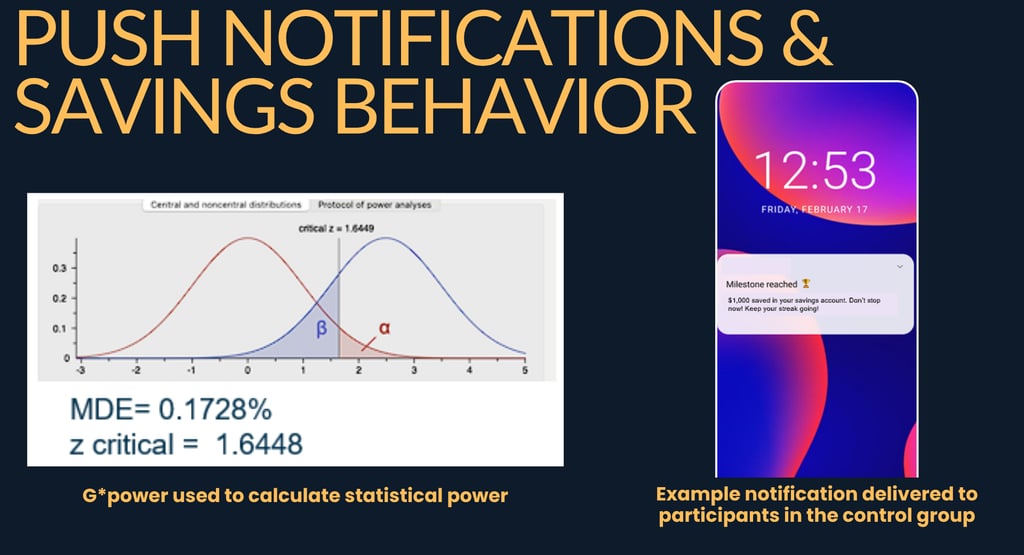

A large-scale A/B experiment was conducted with 2 million users.

Two behavioral interventions were designed and tested:

Achievement framing via milestone notifications.

Soft commitments by prompting users to schedule future deposits.

Users were randomly assigned to control (no message) or treatment (behavioral prompt) groups.

Primary Skills Applied: Hypothesis Testing | Project Management | Stakeholder Management | Statistical Analysis | Data Cleaning | Literature Review

Problem

Despite offering a simple tool for saving and investing, many users were not consistently reinvesting in their savings goals. Driving repeat contributions is critical to long-term customer financial well-being and to the sustainability of this business. The challenge was to increase the recurrence of contributions within their flagship savings account feature.

Potential Applications

Use personalized milestone messages to trigger action.

Embed commitment devices (like deposit scheduling) in success screens or follow-up flows.

Test similar nudges across other financial behaviors (e.g., debt repayment, bill savings).

Limitations

Gains were statistically significant but small in magnitude.

Notification fatigue or timing mismatches may reduce impact.

Treatment focused on behavior initiation but not long-term retention.

External generalizability may be limited to digital-native populations or regions.

Tools Used: R